.png?width=207&height=55&name=Horan_Logo%20Transparent%20No%20Tagline%20(2).png)

If you’re thinking of buying a multi-family house, you might be wondering how to insure it properly. A multi-family house is a property that has more than one unit, such as a duplex, triplex, or fourplex. Each unit can have its own features and amenities, which can affect the cost and coverage of your insurance policy.

We understand that purchasing a multi-family home can bring new challenges and complexities, especially for first-time property owners. For that reason, it’s essential to choose an agent with experience valuing multi-family homes, as they’ll ask the right questions and gather crucial information about your property. Doing this facilitates a policy tailored to your specifically-constructed home.

As an experienced agency, we have a rich history of writing insurance policies for multi-family homes across Central New York. We’re here to guide you through the steps you need to take to make your transition to becoming a landlord a seamless one.

In this article, we will explain the different types of insurance policies for multi-family houses, how to determine the amount of insurance you need, and some of the challenges you might face when insuring a three-family home or above.

We know that one of your biggest concerns as a property owner is the possibility of losing your multi-family house due to a catastrophic event such as a fire or storm.

That’s why we will introduce you to insurance coverage that can help you rebuild your property in case of a total loss.

We will navigate the world of property owner coverage, from homeowners insurance to landlord policies, and discuss the importance of not only covering your property but also ensuring coverage for your tenants.

You’re on the path to being a responsible and well-protected property owner, for which your tenants will be grateful.

So let’s dive in.

Insurance Options for a Multi-Family House

One of the first things you need to consider when buying a multi-family house is whether you will live in one of the units or rent out the entire property. This will determine the insurance policy you need to protect your investment.

If you plan to occupy one of the units, you can get a standard homeowners insurance policy that covers your personal belongings and your liability as a landlord. However, if you plan to rent out all the units, you will need a landlord policy that covers only the structure and your liability, not your personal property.

You should also require your tenants to have their own renters insurance policies to cover their belongings and liability. But more on that a bit later.

Choosing the right type of policy is not enough. You also need to make sure that your policy is written properly and covers the full replacement cost of your multi-family house. The replacement cost is the amount of money it would take to rebuild your property in case of a total loss, such as a fire or a tornado.

The replacement cost may differ from the market value or the purchase price of your property, depending on factors such as construction materials, labor costs, and local building codes.

You should work with an experienced insurance agent who can help you estimate the replacement cost of your multi-family house and adjust your policy limits accordingly. Doing so can help you avoid being underinsured or overpaying for coverage you don’t need.

The Need for Specialized Agents and Policies for Your Multi-Family Home

Multi-family homes come in a variety of architectural styles and designs. Some are converted from large single-family homes originally built in the Victorian or Greek Revival era and later divided into three or four units.

Multi-family homes come in a variety of architectural styles and designs. Some are converted from large single-family homes originally built in the Victorian or Greek Revival era and later divided into three or four units.

Others are purpose-built as two-family homes, such as the ones in the Tipp Hill area. These can be side-by-side duplexes, where each unit has its own entrance and shares a common wall, or two-story homes, where one unit is on the ground floor, and the other is on the upper floor.

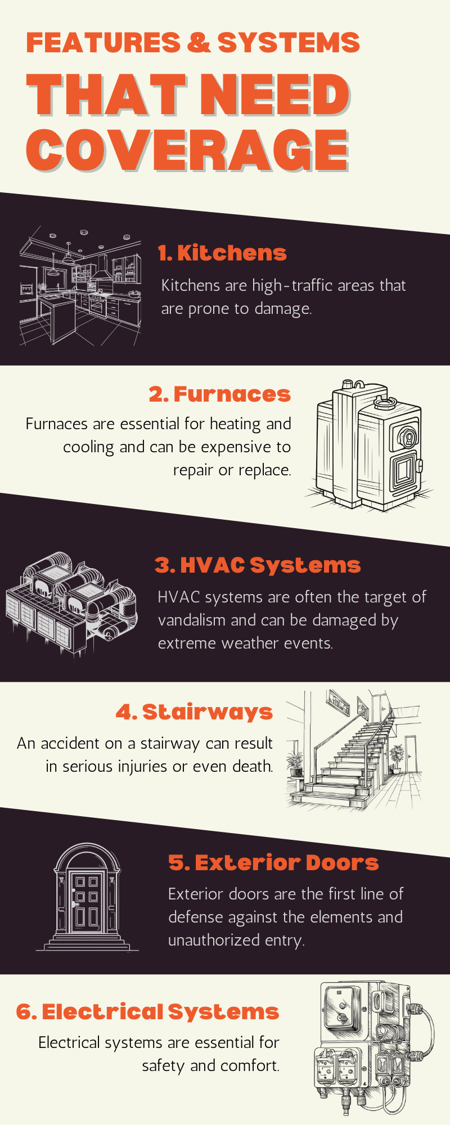

One of the challenges of insuring multi-family homes is that they often have multiple features and systems that need coverage. For example, a multi-family home may have more than one

- kitchen

- furnace

- HVAC system

- stairway

- exterior door, and

- electrical system

These components can increase the value and complexity of the property, as well as the risk of damage or liability. Therefore, it is important to have an accurate inventory of all the features and systems in your multi-family home and make sure they are included in your insurance policy.

You should also inspect and maintain them regularly to prevent any problems or hazards that could affect your insurance claim.

As you can see, multi-family homes have more features and systems than single-family homes, which means they also have higher insurance costs. You don’t want to underestimate the value of your property and end up with insufficient coverage in case of a disaster.

That’s why you need to work with an agent who specializes in multi-family homes and knows how to appraise them correctly. An experienced agent will ask you the right questions and gather the necessary information about your property, such as its age, condition, location, and occupancy. They will also help you find the best carrier and policy for your needs and budget.

The reason why this matters is that you bought a multi-family home for a specific purpose. Whether you want to live in one of the units and rent out the others or rent out the entire property and generate income, you have a vision for your investment. To secure that vision for the future, a primary insurance goal must be met in two steps:

- You want to make sure that if something happens to your property, you can rebuild it as it

was or even better. - To do this, you want to have enough insurance money to cover the full replacement cost of your multi-family home and avoid any financial losses or headaches.

That’s why choosing the right agent and policy is crucial for properly securing your investment, which leads to the ultimate peace of mind.

The Challenges of Insuring Three and Four-Family Homes

If you’re buying a multi-family house with more than two units, you may face some challenges when looking for insurance policies. While two-family homes are common and easy to insure, three and four-family homes are considered riskier by insurance carriers.

This is because they have more tenants, more features and systems, and more potential for claims. Therefore, fewer insurance carriers are willing to offer policies for these types of properties. You should check with your insurance agent early on to see if they have access to carriers that can insure your three or four-family home.

How to Insure a Multi-Family House with More Than Four Units

Another thing to keep in mind is that if your multi-family house has more than four units, it is no longer classified as a residential property. Instead, it falls under the category of commercial property, which requires a different type of insurance policy.

Commercial insurance policies cover the structure and liability of your property but not your personal belongings or the belongings of your tenants. You will also need to consider other factors, such as

- loss of income

- business interruption, and

- detached structures like garages, sheds, and fences

Whether you live in the property or not, you will need a commercial insurance policy for your multi-family house with more than four units. You should discuss the options and requirements with your insurance agent before buying the property.

The Benefits of Requiring Renters Insurance for Your Tenants

As a landlord, you have insurance to protect your property and your liability, but that doesn’t extend to your tenants and their belongings. That’s why you should make renters insurance a condition for renting your units. Renters insurance is a policy that covers the personal property and liability of your tenants in case of a loss or a claim.

Renters insurance can help you and your tenants in several ways:

1. It can cover the liability claims between tenants. If one tenant causes damage or injury to another tenant, their renters insurance can pay for the expenses before you get involved.

For instance, if a tenant starts a fire in their kitchen and the smoke damages the property and belongings of another tenant or causes health problems to their family, the renters insurance of the first tenant can cover the costs.

2. It can replace the tenants’ possessions if they are destroyed. Renters insurance can reimburse the tenants for their personal property if it is damaged or stolen by a covered peril, such as fire, theft, or vandalism.

This way, the tenants don’t have to spend their money to replace their things, which means they can pay their rent on time. This is good for both of you. Renters insurance is not expensive and can be easily obtained from a reputable insurance agent.

A renters policy usually costs less than $10 per month and offers valuable coverage and peace of mind for your tenants. You should recommend prospective tenants to an insurance agent who can advise them on the best policy for their needs and budget. This will benefit them and you as well.

Insure Your Multi-Family Home with Confidence

We understand that buying and insuring a multi-family house can be a daunting task since it involves various considerations and potential challenges. That’s why we stress that enlisting the help of an experienced insurance agent who understands the intricacies of multi-family properties is crucial to ensure proper coverage.

Factors like occupancy, property features, and the number of units will dictate the type of policy and coverage needed. Don’t forget the importance of requiring your tenants to have renters insurance to protect their belongings and liabilities.

If you choose to ignore what we’ve outlined here, you could face serious consequences such as losing your property, paying for damages and injuries, facing legal disputes, and losing income. You could also jeopardize your relationship with your tenants and your reputation as a landlord.

But by taking these steps and working closely with a knowledgeable agent, you can safeguard your valuable investment in a multi-family home without worry.

It’s quite clear that insuring a multi-family house is not a simple task, but it can be done with the right guidance and expertise. Whether you need a homeowners policy, a landlord policy, or a commercial policy, we can help you find the best coverage and price for your property and your tenants.

We have the experience and the knowledge to appraise your multi-family house correctly and tailor your policy to your specific needs and goals. We also have access to insurance carriers that can insure your property, no matter how many units it has.

Once we understand your intended use for the multi-family home, we will recommend the necessary coverage to safeguard against common risks associated with this type of property. As multi-family homes tend to be improperly insured, you can rely on our expertise to avoid such issues.

Don’t hesitate to contact us today for a free quote for your multi-family house. Simply click the Get a Quote button below to get things started. We’re here to make your insurance-buying journey easy and hassle-free.

You’re taking a positive step toward securing your multi-family home. By considering proper insurance, you show that you value your property and tenants.

Not quite ready to purchase a multi-home policy? Stay on the learning curve by reading about the “10 Common Mistakes New Landlords Make When Purchasing Insurance and How to Avoid Them.”

{kind=link}